Buying your first home is one of the biggest financial decisions of your life. For most people, purchasing a property without financial support is difficult, which is why home loans play an important role in making homeownership possible.

However, many first-time buyers feel confused about the home loan process, eligibility, documentation, interest rates, and approval procedures. Understanding how a home loan works can help you avoid mistakes and make smarter financial decisions.

In this complete guide, we will explain the home loan process for first-time buyers step by step, along with important tips to improve your loan approval chances.

What is a Home Loan?

A home loan is a type of financial assistance provided by banks or housing finance companies to help individuals purchase residential property. The borrower repays the loan amount through monthly EMIs (Equated Monthly Installments) over a fixed tenure.

Home loans can be used for:

- Buying a new flat or apartment

- Purchasing an under-construction property

- Buying resale property

- Constructing a house

- Home renovation or extension

Today, multiple banks and financial institutions offer attractive home loan interest rates for first-time buyers.

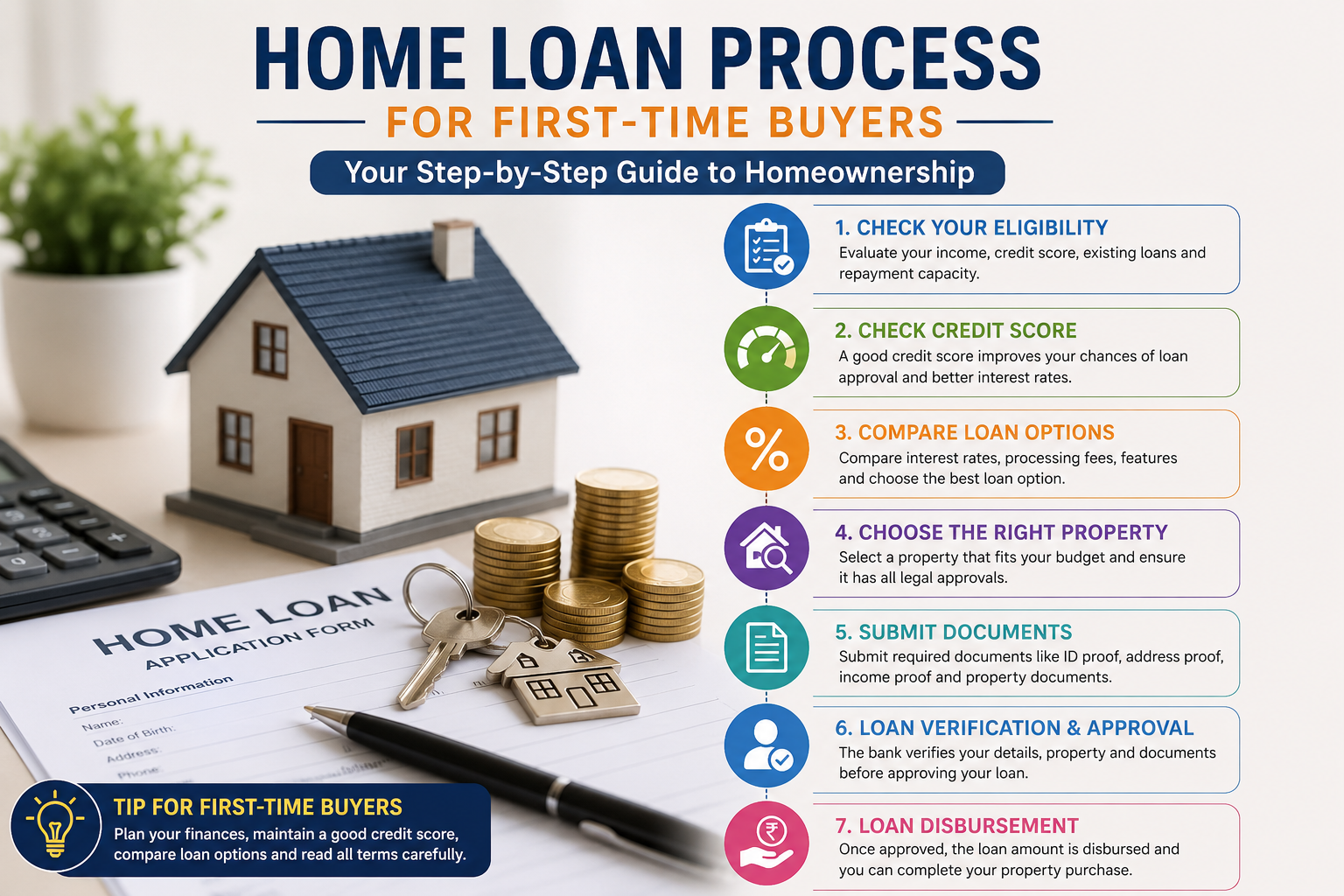

Step-by-Step Home Loan Process for First-Time Buyers

Step 1: Check Your Budget and Eligibility

Before applying for a home loan, you should first understand your financial capacity.

Banks evaluate several factors including:

- Monthly income

- Existing loans

- Credit score

- Employment type

- Age

- Repayment ability

Most banks prefer applicants with:

- Stable income

- Good repayment history

- Credit score above 750

A higher credit score improves your chances of faster approval and lower interest rates.

Step 2: Check Your Credit Score

Your credit score is one of the most important factors in the home loan approval process.

A good credit score shows that you are financially responsible and capable of repaying loans on time.

Tips to improve your credit score:

- Pay credit card bills on time

- Avoid multiple loan applications

- Maintain low credit utilization

- Clear old outstanding debts

Most banks offer better home loan interest rates to borrowers with strong credit profiles.

Step 3: Compare Home Loan Interest Rates

Different banks and housing finance companies offer different interest rates and loan benefits.

Before finalizing a lender, compare:

- Interest rates

- Processing fees

- Loan tenure

- EMI amount

- Prepayment charges

- Customer service

You can choose between:

- Fixed interest rate

- Floating interest rate

Floating rates are generally more popular because they can decrease when market interest rates fall.

Step 4: Choose the Right Property

Banks usually approve loans only for legally verified and approved properties.

Before booking any property, check:

- RERA registration

- Builder reputation

- Legal approvals

- Property documents

- Construction status

If you are buying an under-construction property, make sure the project is RERA approved.

Step 5: Prepare Required Documents

Proper documentation is essential for smooth home loan approval.

Common documents required include:

Identity Proof

- Aadhaar Card

- PAN Card

- Passport

- Voter ID

Address Proof

- Electricity bill

- Passport

- Rental agreement

Income Proof

For salaried individuals:

- Salary slips

- Bank statements

- Form 16

For self-employed individuals:

- Income tax returns

- Business proof

- Profit and loss statement

Property Documents

- Sale agreement

- Builder-buyer agreement

- Property papers

- RERA details

Incomplete documentation may delay loan processing.

Step 6: Loan Application Submission

After selecting the lender and preparing documents, you can submit the home loan application online or offline.

The bank will:

- Verify documents

- Check eligibility

- Evaluate credit score

- Conduct property verification

Some banks may also ask for additional financial documents during the process.

Step 7: Loan Verification and Approval

Once your application is submitted, the lender performs:

- Employment verification

- Income verification

- Credit assessment

- Property legal verification

If everything is satisfactory, the bank issues a sanction letter mentioning:

- Approved loan amount

- Interest rate

- EMI details

- Loan tenure

- Terms and conditions

Carefully read the sanction letter before accepting the offer.

Step 8: Property Verification and Legal Check

The lender conducts a legal and technical evaluation of the property to ensure:

- Ownership is clear

- Property is legally approved

- Construction quality is acceptable

- Market value is appropriate

This step protects both the borrower and the lender from legal complications.

Step 9: Loan Disbursement

After successful verification and agreement signing, the bank disburses the loan amount.

For:

- Ready-to-move properties → Full disbursement may happen immediately.

- Under-construction projects → Payment may happen in stages based on construction progress.

The borrower then starts paying monthly EMIs according to the agreed schedule.

Also Read: Noida Extension vs Ghaziabad: Which is Better for Homebuyers and Property Investment in 2026?

Important Tips for First-Time Home Buyers

Maintain a Good Credit Score

A strong credit score improves approval chances and helps secure lower interest rates.

Avoid Taking Multiple Loans Together

Having too many active loans can reduce your home loan eligibility.

Keep Emergency Savings

Do not invest all your savings in down payment. Maintain an emergency fund for unexpected expenses.

Understand EMI Affordability

Choose an EMI that comfortably fits your monthly budget.

Financial experts generally recommend that total EMIs should not exceed 40–50% of your monthly income.

Verify Property Legally

Always verify:

- RERA registration

- Ownership papers

- Builder credibility

- Land approvals

before making any payment.

Benefits of Home Loans for First-Time Buyers

Home loans offer several advantages including:

- Easy property ownership

- Tax benefits under income tax laws

- Flexible repayment tenure

- Affordable EMIs

- Financial planning support

Many banks also offer special schemes and lower interest rates for women buyers and first-time homeowners.

Common Mistakes to Avoid

First-time buyers should avoid:

- Ignoring hidden charges

- Choosing very high EMIs

- Skipping legal verification

- Applying without checking eligibility

- Ignoring credit score issues

Careful financial planning can help avoid future stress and repayment difficulties.

Final Thoughts

Understanding the home loan process for first-time buyers is extremely important before purchasing property. From checking eligibility and comparing interest rates to verifying property documents and managing EMIs, every step plays a crucial role in successful homeownership.

A home loan can make your dream home affordable, but proper planning, financial discipline, and smart decision-making are essential for a smooth and stress-free experience.

Before applying for a home loan, always compare lenders, understand all charges, and choose a property that fits your long-term financial goals.

FAQs

What is the minimum credit score required for a home loan?

Most banks prefer a credit score of 750 or above for easier approval and better interest rates.

How much down payment is required for a home loan?

Generally, buyers need to pay 10% to 25% of the property value as a down payment.

Can a salaried person easily get a home loan?

Yes, salaried individuals with stable income and good credit scores usually get faster approvals.

Which is better: fixed or floating home loan interest rate?

Floating interest rates are more popular because they can decrease when market rates fall.

Can first-time buyers get tax benefits on home loans?

Yes, homebuyers can claim tax benefits on both principal repayment and interest paid under applicable income tax laws.

Leave a Reply